When a Powerball jackpot hits the news, the headline number is always jaw-dropping. Hundreds of millions. Sometimes over a billion. But once the cameras turn off and the confetti settles, one unavoidable question follows every big win:

How much of that money actually ends up in the winner’s pocket?

The short answer: a lot less than the advertised jackpot. The longer answer is where things get interesting.

The Big Number vs. the Real Payout

Powerball jackpots are announced as annuity values, meaning the full amount is paid out over 30 annual installments, not all at once. Most winners choose the cash option, which immediately cuts the jackpot to roughly 55–60% of the advertised amount.

That reduction happens before taxes are even considered.

For example:

- A $500 million advertised jackpot

- Cash option: roughly $280–300 million

Only after that does the tax bill arrive.

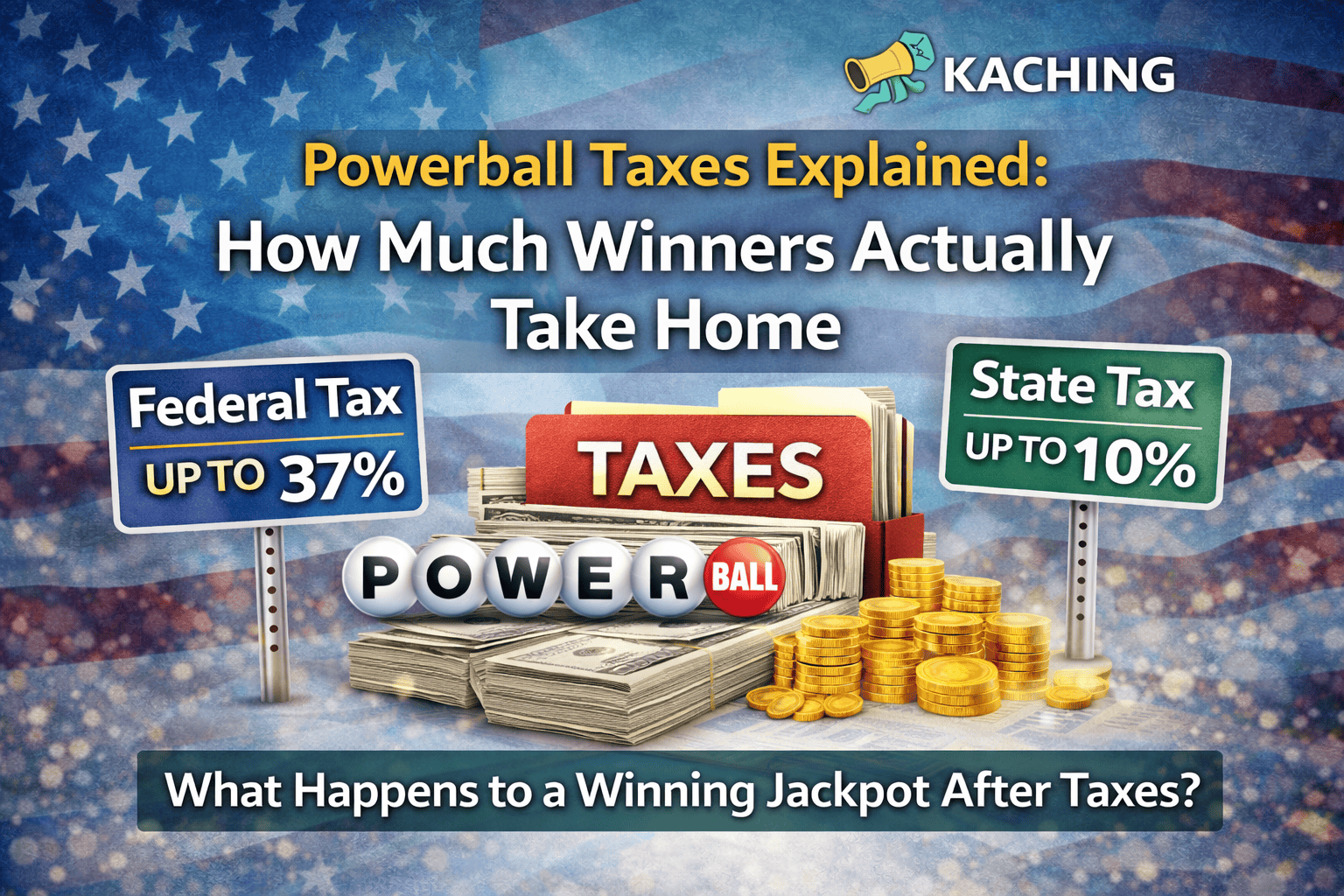

Federal Taxes: The First Major Cut

Under U.S. law, lottery winnings are treated as ordinary income.

That means Powerball winnings are subject to:

- 24% federal withholding immediately

- Up to 37% total federal income tax, depending on the winner’s tax bracket

The 24% withholding happens right away, but it’s not the final bill. High jackpot winners almost always owe more when they file their taxes.

On a $300 million cash payout, federal taxes alone can exceed $100 million.

State Taxes: Where You Live Matters A Lot

State taxes can dramatically change what a winner keeps.

Some states do not tax lottery winnings at all, including:

- Florida

- Texas

- California

- Washington

Other states take a significant share:

- New York: over 10%

- Maryland: around 8.95%

- New Jersey: up to 10.75%

In high-tax states, the combined federal and state tax burden can exceed 45% of the cash payout.

So What Do Winners Actually Keep?

In many real-world cases, a Powerball winner who chooses the cash option ends up keeping between 45% and 55% of the advertised jackpot.

That means:

- A $1 billion jackpot may translate to $450–550 million after taxes

- Still life-changing but far from the headline number

This gap between perception and reality is why financial advisors often say the real story of a Powerball win begins after the ticket is verified.

Why the Tax System Is Structured This Way

Lottery winnings fall into the highest income brackets by default, pushing winners into top federal tax rates. Unlike capital gains, there’s no special tax treatment for lottery prizes.

Governments argue this structure:

- Treats lottery income the same as other windfalls

- Helps fund public programs tied to lottery revenues

- Prevents sudden wealth from being lightly taxed

Whether that feels fair to winners is another debate entirely.

(FAQs) Of Powerball Jackpots Taxes

Can Powerball winners legally reduce their tax bill?

Yes, but only to a degree. Winners often use trusts, charitable donations, and long-term financial planning to manage taxes, though the core federal tax rate cannot be avoided.

Do Powerball winners pay taxes every year if they choose the annuity?

Yes. Each annual payment is taxed as income in the year it is received, which can sometimes reduce the overall tax impact compared to a single large cash payout.

Are lottery winnings taxed differently outside the U.S.?

Yes. Some countries, such as Canada and the UK, do not tax lottery winnings at all, making the U.S. one of the stricter systems globally.